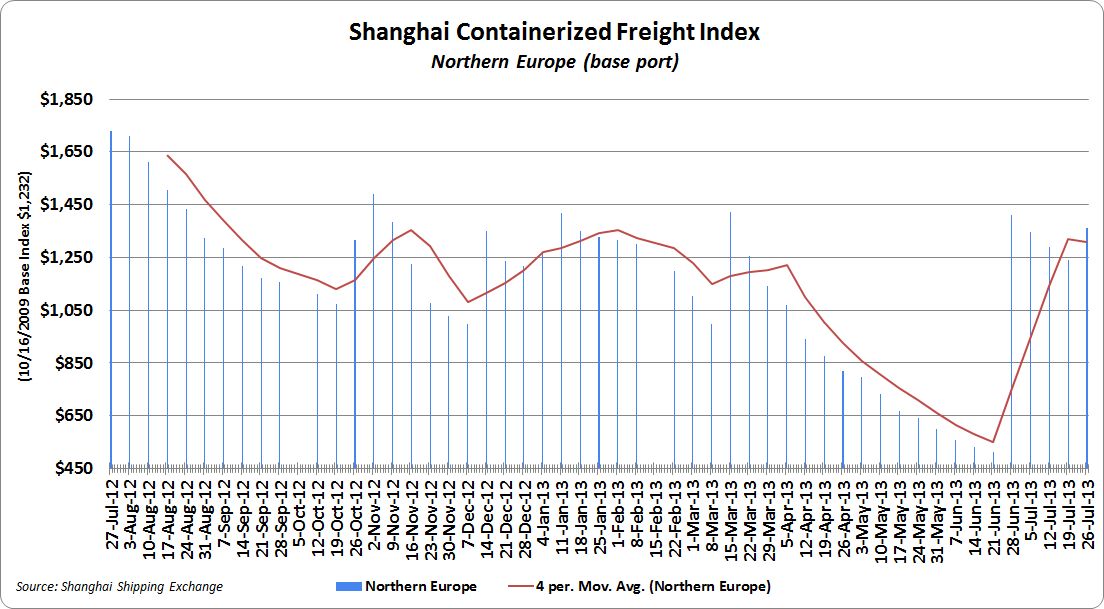

Spot container rates from Asia to northern European ports measured by the Shanghai Containerized Freight Index jumped nearly 10 percent in the week ending July 26.

“It seems as if the reports last week about a lack of capacity on the key Asia-Europe route are beginning to have an effect. The jump in northern European ports can be seen as a strong signal given that the GRI does not fully come into force until Aug. 1. With this in mind and the apparent lack of space, participants are expecting a further jump of around $200 to $300 (per TEU) next week, which would bring the total increase to around $400,” said Richard Ward, research analyst for container derivatives at ICAP.

Most Asia-Europe carriers have proposed a general rate increase in the range of $500 per 20-foot-equivalent unit for Aug. 1. Hanjin Shipping and MOL were the first to announce such increases, and carriers such as OOCL, Mediterranean Shipping Co., Hyundai Merchant Marine, Hapag-Lloyd, Zim Integrated Shipping Services, Cosco and United Arab Shipping Co. have followed suit. Maersk Line announced an increase of $300 per TEU for Aug. 1. NYK Line set a rate restoration for cargo from Asia to Europe for Aug. 10, an increase of $570 per TEU.

Shanghai Containerized Freight Index, North Europe,

Shanghai Containerized Freight Index, North Europe, week ending July 26, 2013

The spot rate from Shanghai to northern European ports increased 9.7 percent or $120 this week to $1,360 per TEU. The spot rate had fallen 12 percent, or $169 per TEU, over the previous three weeks. The current SCFI index to northern Europe is still 21.3 percent below where it was at the same point in 2012, but 7 percent higher than at the beginning of 2013.

The spot rate from Shanghai to Mediterranean ports inched down 0.1 percent in the week to July 26 from the week before to $1,234 per TEU, according to the latest SCFI data issued by the Shanghai Shipping Exchange. Ocean carrier rates have fallen 11 percent or $152 over the past four weeks. The current SCFI index to the Mediterranean is 25.2 percent below where it was at the same point in 2012, but 6.6 percent above where it was on Jan. 1

“Of course as usual there are doubts as to whether the increase can be sustained past the middle of the month and, without further GRIs being announced, the medium- to long-term outlook remains bearish. It is yet to be seen if any of the planned GRI on this route will come into force, and we will have to wait until next week before we categorically say if the increase has been a success or failure,” Ward said.