This key trade, responsible for the industry’s biggest profits and its steepest losses in recent years, also faces a period of uncertainty in the run-up to the planned second quarter launch of the controversial P3 alliance among the world’s top three carriers — Maersk Line, CMA CGM and Mediterranean Shipping Co. — which will account for some 45 percent of total capacity on the route.

The Asia-Europe trade also will be the main focus of the recently launched investigation by European Union competition regulators into suspected illegal collusion by 14 carriers to boost freight rates.

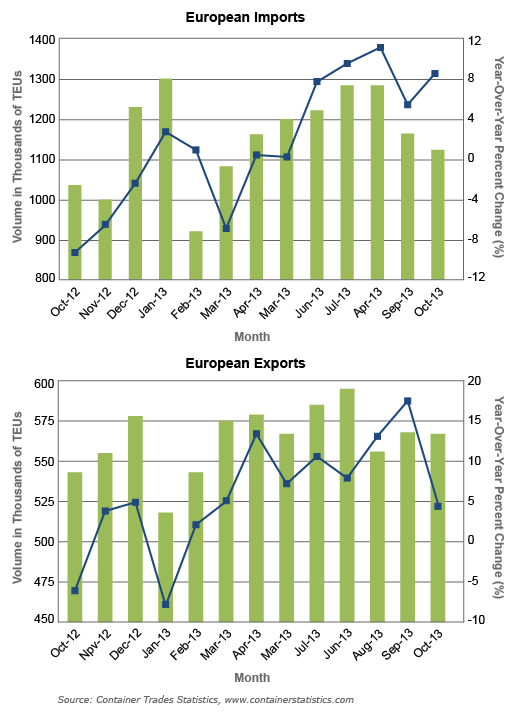

European containerized imports and exports, Oct. 2012 to Oct. 2013

European containerized imports and exports, Oct. 2012 to Oct. 2013Carriers have adjusted to the fact that the days of double-digit growth that spurred massive investments in ships and networks before the 2009 global slump are a thing of the past, and realize the way to make money is through meaningful capacity management and an obsessive focus on cost-cutting as they introduce ever-larger ships.

This is becoming even more critical as growth in Asia-Europe demand falters even as the global market likely will increase by up to 5 percent this year. Volume on the key westbound leg to Europe increased 3.4 percent year-over-year to 10.6 million 20-foot-equivalent units in the first nine months of 2013, buoyed by a rise of more than 8 percent in the third quarter. But this was still down by some 100,000 TEUs from the same period in 2011, according to figures from Container Trades Statistics, a U.K.-based research analyst.

China is the key to the health of the Asia-Europe market, considering it’s the EU’s biggest commercial partners, with two-way trade in goods worth 434 billion euros ($590 billion) in 2012. EU exports to China plummeted by 2 billion euros in the first half of 2013 to 71 billion euros and imports were 7 billion euros lower at 134 billion. Trade is expected to pick up in the coming months, but there are persistent worries that the fragile eurozone recovery could unravel rapidly and China will miss its targeted 7.5 percent growth in GDP in 2014.

It’s not only Asia-Europe’s sluggish demand that’s out of sync with other, growing trade lanes but also its freight rates. CMA CGM’s average revenue per TEU declined 11.8 percent in the third quarter from a year earlier, but its Asia-North Europe rates collapsed a stunning 45 percent.

Some of the largest carriers have responded to the traffic decline in the seasonally weak fourth quarter by canceling sailings, and more suspensions are expected through February. They likely also will lay up tonnage if business deteriorates further early this year.

The arrival of increasingly larger ships, including several more of Maersk’s 18,270-TEU Triple Es through 2014, hasn’t spooked the trade because carriers are largely replacing smaller vessels that have been cascaded to faster-growing north-south routes. The new vessels also have significantly lower unit costs, which should feed through to the bottom line, given effective capacity management.

Cutting costs, particularly in the big-ticket Asia-Europe trade, is key to carriers’ financial health. And the big, well-managed carriers are making enough money across their global networks to blunt the impact of losses on the trade. Maersk Line’s third quarter profit rose to $554 million from $498 million a year earlier, boosted by a 13 percent reduction in unit costs. CMA CGM also stayed in the black in the quarter, although its operating profit fell by almost half to $238 million from $541 million in the third quarter of 2012.

The industry’s attention is fixated by the imminent launch of the P3. But the impact, at least initially, likely will be muted because it won’t swell capacity on the route. The fate of the giant trade will largely be determined by the strategy of market leader Maersk Line. The Danish carrier says it will fight for its 15 percent world market share, including approximately 20 percent of Asia-Europe volumes.

Although the trade is set for further volatility in the short term, there’s no denying its long-term appeal, which recently has been overshadowed by strong growth on north-south and intra-Asia routes. Beijing is pressing Brussels to start talks over a free trade agreement to boost two-way trade to $1 trillion by 2020. The EU is wary of cutting a deal with China for fear it will flood the 28-nation bloc with cheap imports, but in time it’s expected to sit down at the negotiating table.